Connect with NCR-Accredited Experts and Take Control of Your Finances. When monthly payments start to feel overwhelming, debt review can be a lifeline — but only if it’s done right.

Debt Review in South Africa is a formal process created under the National Credit Act to help over-indebted consumers repay what they owe in a more sustainable way. When you shortlist the top 10 debt review companies registered with NCR, you improve your chances of working with professionals who follow the rules, treat you fairly, and communicate clearly. These providers assess your situation, propose a restructured repayment plan, and deal with your creditors within a regulated framework.

Most people consider Debt Review when they are juggling several loans and store accounts, skipping payments, or depending on new credit to cover monthly expenses. A reputable firm will not push you into the process, but will explain the implications, including the impact on access to future credit, before you decide. The aim is steady recovery and better control, not a quick escape from responsibility.

All firms on any serious top 10 debt review companies registered with NCR list should start with a thorough affordability assessment. This includes verifying income, fixed expenses, dependants, and every active credit agreement in your name. Based on this, they can see whether Debt Review is suitable or whether other routes, such as tighter budgeting or informal creditor discussions, might be better.

Once you agree to proceed, a registered debt counsellor will formally notify your creditors and the NCR, and propose new repayment terms. In many cases this means reduced instalments over a longer period, collected via one consolidated monthly debit order. Throughout the process, you should have access to updates, clear statements, and a contact point for questions or changes in your circumstances.

Wealth Creatives is not a debt counselling firm and does not run a Debt Review practice. Instead, our role is to help you navigate the market and connect with NCR-registered partners who have a solid track record and transparent processes. This is especially useful if you are comparing multiple providers and want a neutral view before choosing.

We pre-screen partner firms to confirm their registration status, service offering, and communication standards. This gives you a shorter, safer shortlist when you are weighing up which professionals belong on your personal top 10 debt review companies registered with NCR list. You can complete a quick, no-obligation pre-qualification online or via WhatsApp, and then decide how you want to proceed.

Credit use, cost of living, and employment patterns vary across South Africa, so Debt Review cannot be approached as a one-size-fits-all solution. If you are based in the Western Cape, for example, you may want a provider who understands local employers, housing costs, and municipal billing. Our overview of Debt Review in Cape Town explains how regional insight can support a more realistic repayment proposal.

Elsewhere in the country, similar principles apply: you want a counsellor who listens, adapts the plan to your actual expenses, and stays reachable when circumstances change. Whether you are employed, self-employed, or earning irregular income, the structure of your repayment plan should reflect your real cash flow, not a generic template.

Debt Review is not the only option if you are under pressure. In some cases, especially where arrears are still limited, debt mediation can be a more flexible way to negotiate revised terms directly with creditors. Our overview of debt mediation in South Africa outlines how this differs from the formal Debt Review route and when it might be worth exploring.

A careful comparison of both approaches can help you avoid unnecessary costs or commitments. Decision-makers in households and small businesses should look at the medium-term impact on cash flow, rather than focusing only on immediate relief.

Before you commit to any provider, it is wise to read independent information, compare offerings, and understand the practical day-to-day impact. Our latest guidance and case-based insights are available in the Wealth Creatives articles section, written with South African consumers in mind. This can help you ask stronger questions when you speak to a potential counsellor.

When you are ready to explore your options with an NCR-registered partner, you can reach out through our contact page. A focused conversation upfront will help you decide whether to move forward with Debt Review, consider alternatives, or first make internal changes to your budget and credit use. The goal is a realistic plan that you understand and can stick to over time.

If your financial stress has reached a point where you can’t sleep at night, it’s time to act. Debt review can help you reclaim control, restore confidence, and rebuild your life.

It only takes a few minutes to find out if you qualify.

Start a free WhatsApp chat or complete the contact form and we will call you back.

Wealth Creatives is not a registered debt counselling firm. We connect clients to verified NCR-accredited professionals who provide debt review services in accordance with the National Credit Act.

Debt review is only safe and legal when handled by a National Credit Regulator (NCR) accredited professional. That’s why Wealth Creatives only refers clients to trusted, verified partners who follow strict industry standards and help you understand your financial situation.

Here’s what you gain:

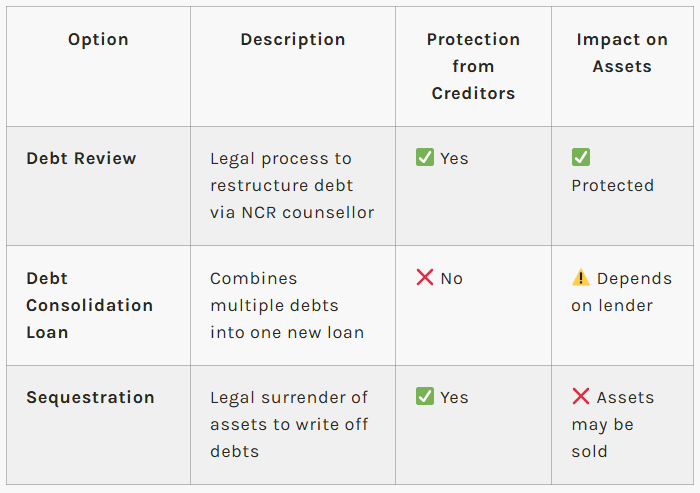

Many people confuse debt review with debt consolidation loans or sequestration. Here’s how they differ:

| Option | Description | Protection from Creditors | Impact on Assets |

|---|---|---|---|

| Debt Review | Legal process to restructure debt via NCR counsellor | ✅ Yes | ✅ Protected |

| Debt Consolidation Loan | Combines multiple debts into one new loan | ❌ No | ⚠️ Depends on lender |

| Sequestration | Legal surrender of assets to write off debts | ✅ Yes | ❌ Assets may be sold |

Find answers to commonly asked questions about debt counselling. We are here to answer all of your questions.

A trained consultant will go through the your budget and advise on the optimal affordable amount which is available to pay credit providers. This amount will be determined after the clients living expenses and those of their dependents, have been accounted for.

Our NCR accredited partners do not recommend that you exclude your home loan from the debt review process. The National Credit Act implemented the inclusion of your home loan in the debt review process, to assist consumers with keeping their homes. The NCA requires that all debt agreements are included in the debt review.

The National Credit Act implemented the inclusion of your home-loan in the debt review process, to assist consumers with keeping their homes. The NCA requires that all debt agreements are included in the debt review. In addition to including your home loan under debt counselling, the following tips should be taken into account and will assist with making sure you are able to pay off your debt in no time.

Reducing interest rates on all current debt repayments, as well as other debt expenses, with the process of debt counselling is a beneficial solution until you have paid off all of your unsecured debts and therefore, it will allow you to go back to your normal home loan repayments.

When under debt counselling it is best to include your home loan as a defined debt repayment on your home loan with being included in the debt review. The debt repayment should either be equal to or approximately 80% of the contractual repayment. This would extend the repayment terms by 20%, making the monthly debt repayment an affordable amount.

Debt counsellors will assess your credit agreements and determine whether you have been a victim of reckless lending. In the event that credit has been recklessly lent to a consumer, a court can be approached in order to declare the debt as reckless and the repayment of that debt will be written off. This will ensure that the client is placed in a better financial position and increase the affordability of their debt.

Debt counsellors will efficiently review your living expenses and financial situation by drawing up an affordable monthly budget and making sure that you have made the maximum amount of your funds available for debt review. This will give credit providers peace of mind, as they will know that a debt counsellor is contributing the consumer’s maximum amount towards settling their debt.

As per the National Credit Act, the credit providers do not have to reduce interest rates. The good news is that many credit providers are willing to reduce interest rates so that a consumer can get out of debt in a reasonable period of time.

As per the National Credit Act (NCA) credit providers do not have to reduce interest rates.

The good news is that many credit providers are willing to reduce interest rates so that a consumer can get out of debt in a reasonable period of time.

If the debt is to be settled in 60 months or under (for unsecured debts such as personal loans, store cards and credit cards) than most credit providers will accept the new payment plan. If the proposed new payment plan is over an excessive period of time, then many creditors will reject the proposal and there will be no reduction in interest rate.

You will remain blacklisted in South Africa as long as the debt is not paid, so it stays there for as long as the debt is owed.

However once the debt is paid in full, then the company that blacklisted you on ITC needs to send a letter to them informing them the debt has been paid & to give permission to remove it.

For the quickest and safest way to remove your blacklisting status in South Africa, enter the debt review process with one of our NCR accredited partners and take your first steps to clearing your name.

No you don’t have to. A formal interview conducted on one of our NCR accredited partners premises is not required in order to purchase a debt solution. Most debt related processes can be handled over the phone, however, certain documents need to be signed by clients and returned to the debt counsellor.

Signing up for an effective and trustworthy debt solution is done over the telephone and via email. This ensures that process is conducted as quickly and conveniently as possible, to save you time and money.

The application process is 100% safe and reliable, as experts financial consultants will assist you every step of the way. All personal and financial information is kept confidential and the appropriate steps are made by the company to make sure the client is protected.

On a daily basis, financial consultants and client services team are available to discuss financial queries and service related topics at any time, thus enabling you to stay on top of your debt situation.

Our NCR accredited partners also ensure that all employees follow the company values; service excellence, pride, growing people, forward thinking, integrity and accountability in order to conduct business in the most effective and ethical way.

Clients should never make any promises or arrangements with a credit provider without first discussing the matter with one of our NCR accredited partners. This tactic is often used by credit provider staff who are working under commission, or by debt collection firms working on behalf of the credit providers.

Why use a debt review solution

Our NCR accredited partners can assure you that we offer excellent service. If you are under debt review with us we would have already negotiated with your creditors on an affordable repayment plan.

To date, they have helped thousands of clients and are currently achieving a 90+% success rate.

If a credit provider or debt collector contacts you, the best option would be to contact one of our NCR accredited partners straight away and we will advise you on the best debt solution for your needs.

Never make any arrangements with a credit provider without discussing it with us first, as this can have a negative impact on your entire repayment plan with the other credit providers.

Be warned by debt collectors

Unfortunately, certain debt collectors will use dishonest and illegal tactics in order to trick you into defaulting on your debt review payments in order to pay them instead.

Be aware as debt collectors may pretend that you are not under debt review or that they have terminated your debt review. They are by no means allowed to take this sort of action.

Therefore, if you are at all concerned or confused at any time whilst under debt review, it is vital that you contact one of our NCR accredited partners.

You are able to move and work overseas, however, our partners insist that clients advise them beforehand. As long as clients continue to make monthly payments, they can stay on the debt repayment plan

The following steps map out the process involved with purchasing an item on credit, applying for a loan, or extending the credit limit on your store card and the actions taken by credit providers and credit bureaus.

The credit process differs according to the type of credit you wish you apply for.

The following steps map out the process involved with purchasing an item on credit, applying for a loan, or extending the credit limit on your store card and the actions taken by credit providers and credit bureaus.

Steps of the credit process

For more assistance with the credit process or any questions with regards to sorting out your financial situation, specifically solving your debt contact ezDebt

Our NCR accredited partners operates nationwide, telephonically or online. For more details click here

However, they have attorneys in every jurisdiction of South Africa. Thus, there is no need to meet with clients in person and all that is needed is the client’s documentation, which we will be used to liaise directly with the banks.

Debt review, Administration and Sequestration are viable debt solutions, however, Debt Review is the only option offered to South African consumers struggling to make their debt repayments are faced with financial difficulty.

Debt review, Administration and Sequestration are viable debt solutions, offered to South African consumers struggling to make their debt repayments are faced with financial difficulty. All debt solutions are implemented through systematic business processes, however, they have several differentiating factors.

Administration:

Administration is a debt solution implemented whereby the client’s current debt instalments are reduced and the credit providers receive a debt repayment once every three months. It is a legal process whereby the debt repayment terms are extended, but the downfall lies with the fact that the process is lengthy and takes much longer than debt counselling.

Sequestration:

Sequestration is another debt solution but is not offered. The process entails selling an individual’s current assets in order to pay off or lessen their current debt. In addition to this, the court will appoint someone to manage the client’s money and thus, it is an expensive process.

Debt Review:

Debt review is a debt management solution implemented in order to assist South African consumers with solving their debt problems. The process of debt review will ensure that the client’s debt repayment plan is extended and their current interest rates are reduced, as a professional ezDebt financial consultant will negotiate with the client’s credit providers. The following information sums up the debt review process:

Debt review, administration and sequestration are all solutions targeted at solving the debt problems South African consumers currently face.

The documents may be an S129 letter informing the client that legal action has started, or a summons has been submitted.

Debt consultants will be able to assist you in taking the right course of action. The documents may be a S129 letter informing the client that legal action has started, or a summons has been submitted. Either way, credit providers cannot start legal action if the client has applied for debt review before they send the S129 letter.

Our partners suggest that clients advise the credit providers that they have applied for debt review in terms of section 86 of the National Credit Act. If the credit providers ask for proof, clients will be able to show them their receipt.

If the credit providers ask for proof, you will be able to show them the receipt. If the credit providers do not desist in this practice, please send a complaint through to www.ncr.org.za.

On many occasions, credit providers sell their books of debt and thus, clients can be harassed by another debt collector. Debt collectors still have to follow the national credit act, therefore allowing clients the right to threaten to report them.